econometron.Models.dynamicsge.linear_dsge

classin theeconometron.Models.dynamicsgemodule

Overview

A Dynamic Stochastic General Equilibrium (DSGE) model describes the decisions of households, firms, and policymakers under uncertainty, subject to market-clearing conditions. A linear DSGE model is the first-order Taylor approximation of the model’s nonlinear equilibrium conditions around a deterministic steady state. The linear_dsge class in econometron.Models.dynamicsge allows specification, solution, and analysis of linear and log-linear DSGE models.

Linearization

Given a nonlinear equilibrium system:

let be the steady state. The linearized system is obtained by a first-order expansion in deviations:

Example (levels) If:

then, around :

- Units: original scale

- Use case: variables can be negative (e.g., interest rate gaps)

Log-Linearization

For positive variables, define the log-deviation:

Apply the Taylor expansion to the logged equations.

Example (logs) If:

then:

- Units: percentage deviations from steady state

- Use case: real, strictly positive variables (e.g., output, capital)

In Practice

- Linearization: use for rates, spreads, gaps.

- Log-linearization: use for real quantities.

class linear_dsge capabilities

- Parse string-based equations

- Compute steady states

- Linearize or log-linearize

- Solve RE systems (Klein(2000))

- Simulate and compute IRFs

- Support for analytical and numerical steady-state and derivative computation

Class Definition

from econometron.Models.dynamicsge import linear_dsge

lineardsge=linear_dsge(

equations=list[str],

variables=list[str],

exo_states=list[str],

endo_states=list[str],

parameters=dict[str, float],

approximation=str,

normalize=bool,

shocks=list[str])Parameters

| Name | Type | Description | Default |

|---|---|---|---|

equations | list[str] | Model equations as strings, must include = and time subscripts (_t, _tp1, _tm1). | None |

variables | list[str] | Variable names (e.g., ['A', 'K', 'C']). | None |

exo_states | list[str] | Exogenous state variables. | None |

endo_states | list[str] | Endogenous state variables. | None |

parameters | dict | Model parameters, e.g., {'sigma': 1.5}. | None |

approximation | str | 'linear' or 'log_linear'. | 'linear' |

normalize | dict | Steady-state normalization values. | {} |

shocks | list[str] | Shock variable names. | None |

Attributes

| Attribute | Type | Description |

|---|---|---|

equations_list | list[str] | Provided equations. |

variables | list[str] | All model variables. |

exo_states | list[str] | Exogenous state variables. |

endo_states | list[str] | Endogenous state variables. |

states | list[str] | Combined exogenous + endogenous states. |

controls | list[str] | Variables not in states. |

parameters | dict | Model parameters dictionary. |

approximation | str | Approximation type. |

normalize | dict | Normalization values. |

shocks | list[str] | Shock variables. |

n_vars, n_equations, n_states, n_exo_states, n_endo_states, n_controls | int | Model dimension counts. |

steady_state | pd.Series | Steady-state values. |

A, B, C | np.ndarray | Jacobian matrices. |

f, p | np.ndarray | Policy and state transition matrices. |

irfs | dict[pd.DataFrame] | Impulse response functions. |

simulated | pd.DataFrame | Simulated data. |

initial_guess | numpy array | Initial guess for steady state. |

Methods

1 - validate_entries()

Purpose: Validates inputs during initialization. It checks:

- Non-empty list of equations containing

=. - Non-empty variables list without duplicates.

- Non-empty parameters dictionary.

- Correct data types for states and shocks.

- Non-empty list of equations containing

Returns:

Trueif valid; otherwise raisesValueErroror issues warnings.

2 - set_new_parameters(params)

Purpose:

Updates model parameters (

self.parameters).Returns:

Prints updated parameters or warns if update fails.

3 - set_initial_guess(initial_guess)

Purpose:

Sets initial guess for steady-state computation.

- If approximation="linear", the exogenous shock is set to 0.

- If approximation="log-linear", the exogenous shock is set to 1.

- You can use normalize = {var: value} to assign a specific value to a given variable.Generally, you don’t need to provide this unless required.

- If

set_initial_guessandguessis not specified, it defaults to an array of ones with length equal to the number of endogenous variables.

Returns:

- Stores as

np.arraycould be checked by :- Example

python lineardsge.initial_guess

- Example

- Raises

ValueErrorif size/type mismatch.

- Stores as

4 - compute_ss(guess=None, method='fsolve', options=None)

purpose

- Computes steady state via numerical optimization,currently suppoting

fsolve. if user didn't specify the initial viaguessorset_initial_guess(),it will default to an array of ones with the same length as the endogenous variables.

Parameters:

guess– Initial guess (defaults to ones).method– Only'fsolve'supported.options– Optimizer options.

Returns:

pd.Seriessteady-state values

5 - approximate(method=None, debug=False)

Purpose:

- Approximates the Rational Expectations (RE) model around its steady state using either analytical or numerical Jacobians.

- Uses

_Analytical_jacobians(symbolic, more stable and parsimonious) or_Numerical_jacobians. - Both functions internally call

_reorder_variables, which reorders variables in the sequence: exo_states → endo_states → controls. - Stores Jacobians as

self.A,self.B,self.C. - Once approximated,The model attribute

approximated = Trueand the model can be solved using the Jacobians. - Note : This method must be called after

compute_ss(). Ifapproximate()is called whenapproximated = True, aWarningis raised to notify that the model is already approximated; users should only call this method once after computing the steady state.

Parameters

method:analyticalornumericaldefault :analyticaldebug:bool, optional- If

True, enables debug mode for more verbose output.

- If

Returns

tuple: (A, B, C)- A – Jacobian matrix associated with expectations

- B – Jacobian matrix associated with current endogenous variables

- C – Jacobian matrix associated with exogenous shocks

6 - solve_RE_model(Parameters=None, debug=False)

Purpose:

Solves the Rational Expectations (RE) model of the form

using Klein’s method (generalized Schur decomposition - Solab.m 2000).

- If

Parametersare provided, the Jacobians are recomputed analytically. - Otherwise, it uses the already stored approximated Jacobians.

- The solution is stored in

self.f(policy function) andself.p(state transition function). - This function can be used once The model is approximated.

- If

Parameters

Parameters(dict, optional): Model parameters to override.debug(bool, optional): If True, enables debug mode for more verbose output.

Returns

tuple: (F, P)F – Control function, mapping states to controls:

P – State transition function, governing the law of motion:

7 - _compute_irfs(T=51, t0=1, shocks=None, center=True, normalize=True)

Purpose:

- Computes impulse response functions (IRFs) for a DSGE model, adjusted to match the behavior of the impulse method. IRFs describe the dynamic response of model variables to exogenous shocks.

- Simulates the model’s response to specified shocks over T periods.

- Stores results in self.irfs as a dictionary of DataFrames, with each key corresponding to a shock and its associated IRFs.

- Ensures compatibility with log-linear or linear approximations, with options to

center(return deviations) ornormalize(divide by steady state).

Parameters:

T (int, optional): Number of periods for IRF computation (default: 51).t0 (int, optional): Time period when shocks are applied (default: 1).shocks (dict, optional): Dictionary of shock names and magnitudes. If None, applies a 0.01 shock to each defined shock (default: None).center (bool, optional): If True, returns deviations from steady state; if False, returns levels or log levels (default: True).normalize (bool, optional): If True, normalizes linear approximation IRFs by steady state values(default: True).

Returns:

dict: Dictionary where keys are shock names and values arepd.DataFrameobjects containing IRFs for states, controls, and the shock itself.Notes:

- Requires

f(policy function) andp(state transition function) to be defined. - Raises

ValueErrorif model matrices or shocks are undefined. - Warns if normalization is requested but steady state contains zeros, setting

normalizetoFalse.

- Requires

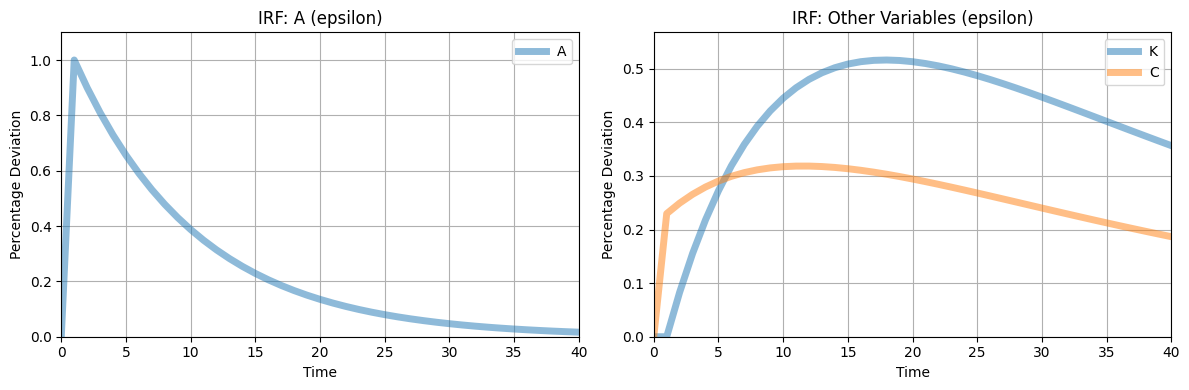

8 - plot_irfs(shock_names=None, T=41, scale=100, figsize=(12, 4), lw=5, alpha=0.5, title_prefix="IRF", ylabel="Percentage Deviation")

Purpose:

Compute impulse Responses via

_compute_irfs()which are stored inself.irfs.Plots impulse response functions (IRFs) for specified shocks, with separate subplots for the corresponding exogenous state and other variables.

Generates a two-panel plot for each shock: one for the exogenous state,

exo_states, and one for all other variables (states and controls).Scales IRF values for better visualization and allows customization of plot aesthetics.

Parameters:

shock_names (list, optional): List of shocks to plot. If None, plots all shocks in self.irfs (default: None).T (int, optional): Number of periods for IRF computation if not already computed(default: 41).scale (float, optional): Scaling factor for IRF values(default: 100).figsize (tuple, optional): Figure size as (width, height) in inches(default: (12, 4)).lw (float, optional): Line width for plots (default: 5).alpha (float, optional): Line transparency (default: 0.5).title_prefix (str, optional): Prefix for subplot titles (default: "IRF").ylabel (str, optional): Y-axis label (default: "Percentage Deviation").

Returns:

None: Displays the plots for each shock. Notes:- Raises

ValueErrorifself.irfsis empty, not a dictionary, or if specified shocks/columns are missing. - Automatically adjusts y-axis limits for clarity.

- Raises

9 - simulate(T=51, drop_first=300, covariance_matrix=None, seed=None, center=True, normalize=True)

Purpose:

- Simulates the DSGE model dynamics over

Tperiods, adjusted to match the behavior ofstoch_sim. Generates stochastic paths for states and controls driven by exogenous shocks. - Discards

drop_firstinitial periods to eliminate transient dynamics. - Supports custom covariance matrices for shocks or defaults to a diagonal matrix based on shock variances.

- Stores results in

self.simulatedas aDataFrame.

- Simulates the DSGE model dynamics over

Parameters:

T (int, optional): Number of periods to simulate (default: 51).drop_first (int, optional): Number of initial periods to discard (default: 300).covariance_matrix (array-like, optional): Covariance matrix for shocks(n_shocks x n_shocks). If None, uses a diagonal matrix with variances of0.01²(default: None).seed (int, optional): Random seed for reproducibility (default: None).center (bool, optional): IfTrue, returns deviations; if False, returns levels or log levels (default: True).normalize (bool, optional): IfTrue, normalizes linear approximation simulations by steady state (default: True).

Returns:

pd.DataFrame: DataFrame containing simulated shocks and variables (states and controls).Notes:

- Requires

self.fandself.pto be defined (model must be solved). - Raises

ValueErrorif model matrices are undefined or covariance matrix has incorrect dimensions. - Warns if normalization is requested but steady state contains zeros, setting

normalizetoFalse.

- Requires

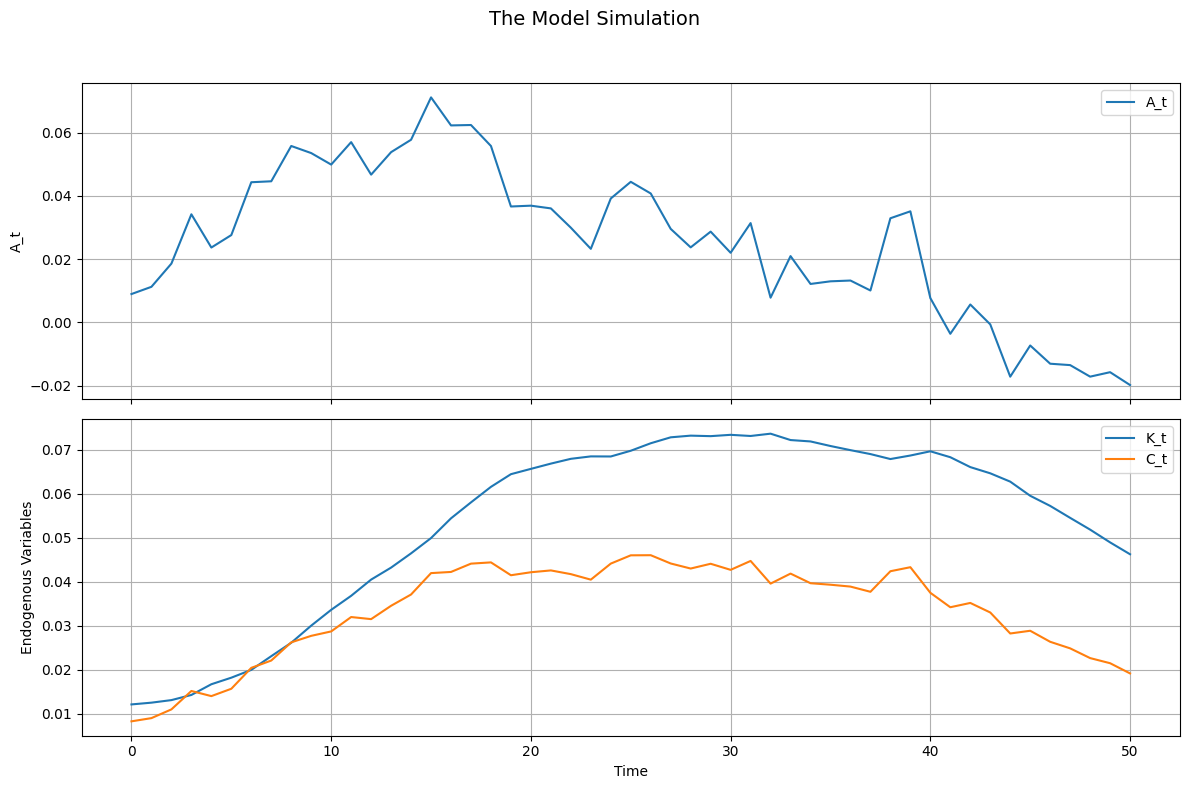

10 - simulations(title="The Model Simulation", figsize=(12, 8), save_path=None)

- Purpose:

Plots the simulated data from simulate, with exogenous states in separate subplots and endogenous variables (states and controls) together in one subplot.

Creates a multi-panel figure where each exogenous state has its own subplot, and all endogenous variables are plotted together.

Allows saving the plot to a file or displaying it.

Parameters:

title (str, optional): Title of the plot (default: "The Model Simulation").figsize (tuple, optional): Figure size as (width, height) in inches (default: (12, 8)).save_path (str, optional): File path to save the plot (e.g., 'plot.png'). IfNone, displays the plot (default: None).Returns:

None: Displays or saves the plot.- Notes:

- Requires

self.simulatedto be apd.DataFramefrom a prior call tosimulate. - Raises

ValueErrorifself.simulatedis not defined or no exogenous/endogenous variables are found. - Automatically adjusts layout to accommodate the title and subplots.

- Requires

Usage Example – RBC Model

1 We Start By importing The class linear_dsge from the econometron.Models.dynamicsge module.

from econometron.Models.dynamicsge import linear_dsge2 We Define The Model Equations as Follow ,specify all the variables, the exogenous , endogenous states and shocks along with the parameters.

equations = [

"-C_t**(-sigma) + beta * C_tp1**(-sigma) * (alpha * A_tp1 * K_tp1**(alpha-1) + 1 - delta) = 0",

"C_t + K_tp1 - A_t * K_t**alpha - (1 - delta) * K_t = 0",

"-log(A_tp1) + rho_a * log(A_t) + epsilon = 0",

]

variables = ['A', 'K', 'C']

exo_states = ['A']

endo_states = ['K']

shocks = ['epsilon']

parameters = {

'sigma': 1.5,

'beta': 0.99,

'alpha': 0.35,

'delta': 0.025,

'rho_a': 0.9,

}

RBC = linear_dsge(

equations=equations,

variables=variables,

exo_states=exo_states,

endo_states=endo_states,

shocks=shocks,

parameters=parameters,

approximation='log_linear',

normalize={'A': 1}

)3 Once our Model RBC is defined, we can proceed with the following steps: we begin by set our initial guess for the computation of the steady-state. Since we have only 1 exo_state and using a simple guess, we can do:

RBC.set_initial_guess([1, 1])

RBC.compute_ss(method='fsolve', options={'xtol': 1e-8}) Steady-state residuals: [-1.77851329e-13 9.03721542e-14 -1.00000000e-02]

Warning: Large steady-state residuals detected.

A 1.000000

K 34.398226

C 2.589794

dtype: float644 Approximating The model around its steady state

RBC.approximate(method='analytical') (array([[-8.33790428e-03, 1.57555735e-04, 1.38972249e-01],

[ 0.00000000e+00, -1.00000000e+00, 0.00000000e+00],

[ 1.00000000e+00, 0.00000000e+00, 0.00000000e+00]]),

array([[ 0. , 0. , 0.13897225],

[-3.44974994, -1.01010101, 1. ],

[ 0.9 , 0. , 0. ]]),

array([[0.],

[0.],

[1.]]))5 Solving The model :

RBC.solve_RE_model()

print("Policy Function (f):\n", RBC.f)

print("State Transition (p):\n", RBC.p) Policy Function (f):

[[0.59492193 0.03861978]]

State Transition (p):

[[0.9 0. ]

[2.85482802 0.97148123]]6 Plotting Impulse Responses

RBC.plot_irfs()

7 Simulations

RBC.simulate(T=51, drop_first=10)8 Plotting The simulations

RBC.simulations()

Notes

- Equation Syntax – Must use time subscripts (

_t,_tp1). - Log-Linear Approximation – Requires non-zero steady-state values.

- Shocks – If omitted, model is deterministic.

- Normalization – Overrides steady-state values for log-linear models.

Limitations

- Only

'fsolve'supported for steady states.